Titan Secures More Trump Funding to Supply 50% of U.S. Graphite Demand

Titan Mining Announces Strong Kilbourne Graphite Project Economics and Expanded U.S EXIM Support to Accelerate U.S. Graphite Independence

December 01, 2025 06:00 ET | Source: Titan Mining Corporation

Poised to be able to Supply Up to 50% of U.S. Natural Graphite Demand with Federal Backing Under EXIM’s “Make More in America” Initiative

After-Tax NPV(7%) of $513 million, 37% IRR, and 2.7-Year Payback

GOUVERNEUR, N.Y., Dec. 01, 2025 (GLOBE NEWSWIRE) — Titan Mining Corporation (TSX:TI, NYSE-A:TII), (“Titan” or the “Company”) an existing zinc concentrate producer in upstate New York and an emerging natural flake graphite producer (a key component of the broader rare earths and critical minerals ecosystem), today announced positive results from its Preliminary Economic Assessment for the Kilbourne Graphite Project (the “Kilbourne Project Study”) and expanded strategic support from the Export Import Bank of the United States (“EXIM”) under the Make More in America (“MMIA”) initiative.

The Kilbourne Project Study confirms robust economics for the project, with an after-tax NPV(7%) of $513 million, 37% IRR, and 2.7-year payback. In parallel, EXIM has approved an additional $5.5 million of non-dilutive MMIA funding, on similar terms as previously announced, to accelerate feasibility work at Kilbourne (the “Feasibility Study”). EXIM has also issued a non-binding Letter of Interest (“LOI”) for up to $120 million of project financing, expected to fund the majority of construction capital, subject to customary due diligence and approvals.

All dollar amounts are stated in U.S. dollars unless otherwise noted.

Highlights

- Critical Materials Complex: Titan’s Empire State Mines in New York State is evolving into a multi-metal critical materials complex, anchored by zinc and graphite, with germanium testing underway that could further strengthen the site’s role in U.S. defense and semiconductor supply chains.

- Robust Economics: After Tax NPV(7%) for the stand-alone Kilbourne Graphite Project of $513 million, post-tax IRR of 37%, and 2.7-year payback, confirming Kilbourne to be the highest return graphite project in the USA.

- High Margins: Average EBITDA of $125 million through LOM. Blended EBITDA margins of 58-69% supporting resilient returns across market cycles.

- Scale & Impact: Average production of ~40,000 metric tonnes per annum of graphite concentrate, at nameplate capacity, nearly 50% of current U.S demand, from an integrated operation in New York State.

-

Expanded United States Government partnership:

- EXIM has approved an additional $5.5 million of non-dilutive funding under MMIA, on similar terms as previously announced, to accelerate resource drilling, metallurgical test work, and engineering work programs for the Feasibility Study. This is the first Feasibility Study for a domestic project funded by EXIM, underscoring the strategic importance of fast-tracking Kilbourne.

- EXIM has also issued a $120 million LOI expected to cover the majority of the construction capital, materially de-risking financing and underscoring the Project’s strategic role in U.S. national security and defense supply chains.

- Capital Efficiency: Initial construction capital of $156 million, leveraging existing Empire State Mine infrastructure, government financing programs, and cash flow from Titan’s zinc operations to minimize dilution and execution risk.

- Product Strategy: Initial output of Concentrate, Micronized Natural Flake Graphite (NFG), and Purified Micronized Graphite (PMG), with transition to Coated Spherical Purified Graphite (CSPG), all critical inputs for industrial, defense and energy sectors.

- Significant Exploration Upside: The Kilbourne Project Study is underpinned by an Inferred Mineral Resource of 22.4 million tons grading 2.91% Cg (653,000 tons contained graphite), based on a 1.5% Cg cut-off grade. Significant exploration upside remains, with only 30% of the known strike length drilled to date.

- Near-Term Production Pathway: Qualification sales production commencing in Q4 2025 with customer qualifications commencing Q1 2026. The demonstration facility significantly de-risks the Kilbourne Project, accelerates time-to-market, and provides early validation of Titan’s downstream processing strategy.

- Fast Tracking Development: Feasibility Study in 2026 with targeted start of construction in 2027.

- Job creation & economic impact: Project expected to create approximately 160 additional permanent positions, establishing a total workforce of over 300 employees across ESM operations in upstate New York, while generating tax revenue and local economic benefits for St. Lawrence County and New York State.

- Zinc operations: Ongoing production from the Empire State Mine provides cash flow stability, with production expected to grow incrementally. Exploration potential across Titan’s land package and operational synergies with the Kilbourne Project further enhance value and reduce execution risk.

John Jovanovic, Export-Import Bank of the United States, said: “This investment demonstrates EXIM’s commitment to strengthening domestic supply chains for strategic minerals essential to our national security and economic prosperity. Titan’s innovative approach to developing America’s first integrated graphite capability in more than 70 years aligns directly with our mission to support U.S. jobs and reduce foreign dependencies in critical sectors.”

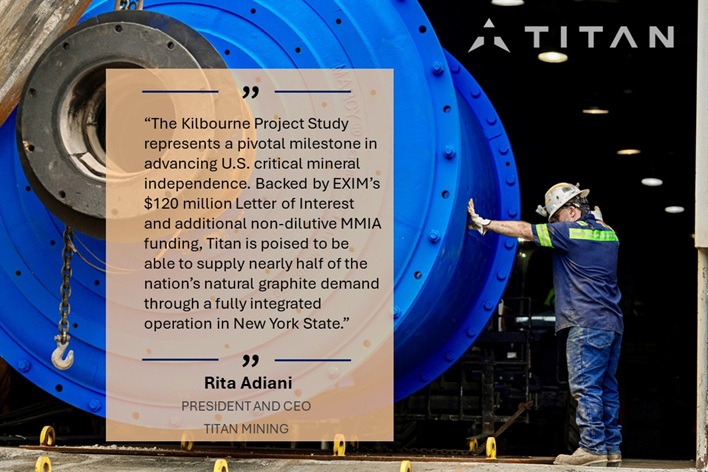

“The Kilbourne Project Study represents a pivotal milestone in advancing U.S. critical mineral independence,” said Rita Adiani, CEO and President of Titan Mining. “Backed by EXIM’s $120 million Letter of Interest and additional non-dilutive MMIA funding, Titan is poised to be able to supply nearly half of the nation’s natural graphite demand through a fully integrated operation in New York State.”

Adiani continued, “EXIM’s support is far more than capital—it is validation of Titan’s strategic role in establishing America’s graphite independence. By providing non-dilutive funding at the feasibility stage and confirming project-finance support for construction, EXIM is enabling Titan to move faster while preserving balance-sheet strength. Together with our established zinc operations generating cash flow, we are building a U.S.-anchored critical minerals platform with clear, long-term growth.”

Cautionary Note: The Kilbourne Project Study is preliminary in nature and includes Inferred Mineral Resources, considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as Mineral Reserves, and there is no certainty that the Preliminary Economic Assessment will be realized. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability.

Project Summary

The Kilbourne Project hosts a maiden Inferred Mineral Resource of 22.4 M tons grading 2.9% Cg, with significant expansion potential as only ~30% of the strike length has been drilled. Development is planned as a conventional open-pit mine with an average annual production of ~40,000 metric tonnes of graphite concentrate (at nameplate capacity). Processing will use a flotation-based concentrator, achieving 95% Cg at ~90% recovery, with downstream secondary transformation facilities to produce high-purity micronized and spherical graphite for battery applications. Co-located within Titan’s Empire State Mine complex in New York, the project benefits from established infrastructure, utilities, and a skilled workforce. Work completed to date includes drilling, metallurgical testing, and construction of a demonstration plant to begin customer qualification in 2026.

Based on the positive Kilbourne Project Study results, Titan will advance the project to feasibility, supported by additional drilling, expanded metallurgical testing, site-specific engineering, and environmental permitting programs. Pilot-scale purification and downstream test work will generate product samples to secure offtake agreements, further de-risking commercialization and positioning Kilbourne as a cornerstone of U.S. graphite supply.

Table 1: Operational Parameters of the Kilbourne Project Study

| Operational Parameters | Value |

|---|---|

| LOM (Life of Mine) | 13 years |

| Nominal annual processing rate | ~1.39 M tonnes |

| Stripping ratio (LOM) | 2.15:1 |

| Average grade (LOM) | 2.84% Cg |

| Average graphite recovery | ~90% |

| Average annual graphite concentrate & value-added production (LOM) | 37,438 tonnes |

Table 2: Economic Highlights of the Kilbourne Project Study

| Economic Highlights | Value |

|---|---|

| Pre-tax NPV (7% discount rate) | $581 M |

| After-tax NPV (7% discount rate) | $513 M |

| Pre-tax IRR | 38.9% |

| After-tax IRR | 37.0% |

| Pre-tax payback | 2.66 years |

| After-tax payback | 2.69 years |

| Initial CAPEX | $156 M |

| Expansion CAPEX | $176 M |

| Sustaining CAPEX | $100 M |

| LOM OPEX | $886 M |

| Annual OPEX | $68 M (avg.) |

| OPEX per tonne of salable products: | |

| STD Purity Flake Concentrate | $990 |

| STD Purity Micronized Flake Grades | $1,197 |

| High Purity Micronized Flake Grades | $2,233 |

| CSPG Anode Grades | $3,612 |

| Avg. EBITDA | $125M |

Table 3: Commodity Input Pricing

| Products | Weighted Average Sale Price ($/t) |

|---|---|

| STD Purity Flake Concentrate (95.0% LOI MIN) | 1,575 |

| STD Purity Micronized Flake Grades (95.0% LOI MIN) | 3,770 |

| High Purity Micronized Flake Grades (99.9% LOI MIN) | 5,185 |

| CSPG Anode Grades (99.95% LOI MIN) – year 5 | 11,193 |

Table 4: Initial, Expansion and Sustaining Capital Costs

| Project Area | Total ($K) | Initial ($K) | Expansion ($K) | Sustaining ($K) |

|---|---|---|---|---|

| Open Pit Mine | 41,641 | – | – | 41,641 |

| Site Infrastructure & TMF | 46,150 | 27,241 | – | 18,909 |

| Concentrate Plant | 115,922 | 72,610 | – | 43,312 |

| Micronization Plant | 22,362 | 11,497 | 10,865 | – |

| Purification Plant | 13,311 | 5,291 | 8,020 | – |

| CSPG Plant | 99,477 | – | 99,477 | – |

| Closure & Salvage | -4,065 | – | – | -4,065 |

| Direct Costs | 334,799 | 116,639 | 118,362 | 99,798 |

| Owner’s Cost & Indirects | 49,939 | 15,792 | 33,900 | 247 |

| Contingency | 47,000 | 23,328 | 23,672 | – |

| Total | 431,738 | 155,759 | 175,934 | 100,045 |

Table 5: Project All-in Operating Costs

| Project Area | LOM Total ($K) | Remaining Concentrate ($/t) | Micronized NFG ($/t) | PMG ($/t) | CSPG ($/t) |

|---|---|---|---|---|---|

| Open Pit – Kilbourne Mining | 183,832 | 378 | 389 | 414 | 563 |

| Site Infrastructure – G&A | 47,077 | 97 | 100 | 106 | 144 |

| TMF | 11,178 | 23 | 24 | 25 | 34 |

| Concentrate Plant | 239,677 | 492 | 508 | 539 | 734 |

| Micronization Plant | 75,647 | – | 176 | 186 | 228 |

| Transport | 21,694 | – | – | 80 | 108 |

| Purification | 107,222 | – | – | 883 | – |

| CSPG Plant | 199,610 | – | – | – | 1,801 |

| Operating Costs | 885,936 | 990 | 1,197 | 2,233 | 3,612 |

Table 6: Kilbourne Graphite Mineral Resource Summary

| Classification | Deposit | Cut-off Grade (% Cg) | Tonnage (‘000 tons) | Grade (% Cg) | Contained Graphite (‘000 tons) |

|---|---|---|---|---|---|

| Inferred | Kilbourne | 1.50 | 22,423 | 2.91 | 653 |

The independent Qualified Person for the Mineral Resource Estimate, as defined by NI 43-101 is Mr. Todd McCracken (PGO 0631) of BBA USA Inc. The effective date of this Mineral Resource Estimate is December 3, 2024.

Three-dimensional (3D) wireframe models of mineralization were based on the geological interpretation of the logged lithology and sub-domained based on contiguous grade intervals greater than or less than 0.50% Cg defining two mineralized sub-domains.

Geological and block models for the Mineral Resource Estimate used data from a total of 45 surface diamond drill holes (core) and 1 surface channel sample. The drill hole database was validated prior to mineral resource estimation and QA/QC checks were made using industry-standard control charts for blanks and commercial certified reference material inserted into assay batches by Empire State Mine personnel.

Quantities and grades in the Mineral Resource Estimate are rounded to an appropriate number of significant figures to reflect that they are estimations.

The mineral resource estimate was constrained using the following optimization parameters, as agreed upon by Empire State Mine and the QP. The parameters include mining costs of $4.60/ton for mineralized rock, $3.50/ton for unmineralized rock, and $2.00/ton for overburden and tailings, with a 5.0% dilution and 95.0% mining recovery. Processing costs are $14.00/ton milled, with a 91.0% processing recovery and a concentrate grade of 95.0%. No general and administrative (G&A) costs were applied. The selling price is $1,090/ton of concentrate, with transportation costs of $50/ton and no additional selling costs. The overall slope angles are 23 degrees for overburden and tailings, and 45 degrees for rock.

Process recovery estimates based on Phase I testing done at SGS Lakefield and Forte Dynamics, open circuit recovery 86.5% with expected increase to 90-91% in closed circuit.

The reported mineral resource estimate has been tabulated in terms of a pit-constrained cut-off value of 1.50% Cg.

The block model was prepared using Datamine Studio RM™. A 30 ft x 30 ft x 15 ft block model was created, and samples were composited at 5.00 ft intervals. Grade estimation for graphite used data from drill hole data and was carried out using Ordinary Kriging (OK), Inverse Distance Squared (ID2), and Nearest Neighbor (NN) methods. The OK methodology is the method used to report the mineral estimate statement.

Grade estimation was validated by comparison of the global mean block grades for OK, ID2, and NN by domain and composite mean grades by domain, swath plot analysis, and by visual inspection of the assay data, block model, and grade shells in cross-sections.

The specific gravity (SG) assessment was carried out for all domains using measurements collected during the core logging process. The mean specific gravity value within the mineralized domains is 2.75.

The Mineral Resource Estimate was prepared following the CIM Estimation of Mineral Resources & Mineral Reserves Best Practice Guidelines (November 29, 2019).

Use of Proceeds from Expanded EXIM MMIA Support

The additional $5.5 million approved by EXIM under its MMIA initiative will fund critical-path activities to accelerate the Kilbourne Project, including:

- Resource Drilling – to grow the mineral resource base and improve confidence in the existing Inferred Mineral Resource.

- Metallurgical & Product Qualification Work – to refine flowsheets and qualify multiple downstream product categories, including micronized and purified graphite grades for battery, industrial, and defense applications.

- Engineering, Permitting and Site Management Plans – to advance feasibility-level design, de-risk construction, and align project development with U.S. federal procurement and permitting requirements.

This funding is non-dilutive to Titan shareholders and is on the same terms as previously announced MMIA support.

Technical Disclosure

The Preliminary Economic Assessment was prepared by Donald R. Taylor, MSc, PG; Todd McCracken, P. Geo.; Bahareh Asi, P. Eng., David Willock, P. Eng.; Deepak Malhotra, SME Registered Member; Oliver Peters, MSc, P.Eng.; Derick de Wit, FAusIMM; and Steven M. Trader, PG, CPG, each of whom is a “Qualified Person” as defined by NI 43-101. All are independent of Titan, other than Mr. Donald Taylor, who is on Titan’s board of directors. The effective date of the Preliminary Economic Assessment is December 1, 2025, and an NI 43-101 technical report in respect of the Preliminary Economic Assessment will be filed on the Company’s SEDAR+ profile at www.sedarplus.ca and on Titan’s website within 45 days. The scientific and technical information contained herein has been reviewed and approved by the aforementioned Qualified Persons.

Quality Assurance, Quality Control and Data Verification

Core drilling was completed using ESM owned and operated drills which produced AWJ (1.374 in) size drill core. All core was logged by ESM employees. The core was washed, logged, photographed, and sampled. All core samples were cut in half, lengthwise, using a diamond saw with a diamond-impregnated blade and sampled on 5 ft intervals with adjustments made to match geological contacts. After a sample is cut, one half of the core was returned to the original core box for reference and long-term storage. The second half was placed in a plastic or cloth sample bag, labeled with the corresponding sample identification number, along with a sample tag. All sample bags were secured with staples or a draw string, weighed and packed in shipping boxes. Shipping boxes are placed onto pallets and shipped by freight to SGS Lakefield laboratory in Lakefield, ON, Canada for sample preparation and graphitic carbon analysis. Pulps are forwarded to SGS Burnaby laboratory in Burnaby, BC, Canada for multi-element analysis. SGS Lakefield is a Canadian accredited laboratory (ISO/IEC 17025) and independent of ESM. SGS Lakefield prepares the pulps and analyzes each sample for graphitic carbon (Cg-CSA06V) with a detection limit of >0.01%. Pulps are shipped to SGS Burnaby for multi-element analysis by aqua regia digestion (GE-ICP21B20 for 34 elements) with an ICP – OES finish. All samples in which silver, calcium, manganese, iron, zinc and sulfur exceed their upper limit are re-run using methods of aqua regia digestion (Fe-ICP21B100), four acid digestion (Ag, Ca, Zn, and Mn-ICP42Q100) and infrared combustion (S-CSA06V) with the elements reported in percentage (%). Standards and blanks are inserted during the logging process. The assays for QA/QC samples are reviewed as certificates are received from the laboratory. Failures are identified on a batch basis and followed up as required. The scientific and technical information disclosed herein has been verified by Todd McCracken of BBA USA Inc., using data validation and quality assurance procedures under high industry standards. The verification activities included a search for factual errors, completeness of the lithological and assay data, and suitability of the primary data. As part of the database verification activities, the assay information and certificates obtained directly from the analytical laboratory have been examined as well. Mr. McCracken has not identified any legal, political, environmental, or other risks that could materially affect the potential development of the mineral resources disclosed herein.

About Titan Mining Corporation

Titan is an Augusta Group company which produces zinc concentrate at its 100%-owned Empire State Mine located in New York state. Titan is also an emerging natural flake graphite producer and targeting to be the USA’s first end to end producer of natural flake graphite in 70 years. Titan’s goal is to deliver shareholder value through operational excellence, development and exploration. We have a strong commitment towards developing critical minerals assets which enhance the security of the domestic supply chain. For more information on the Company, please visit our website at www.titanminingcorp.com.

Media & Investor Contact

Irina Kuznetsova

Director, Investor Relations

Phone: (778) 870-7735

Email: info@titanminingcorp.com

Cautionary Note Regarding Forward-Looking Information

Certain statements and information contained in this new release constitute “forward-looking statements”, and “forward-looking information” within the meaning of applicable securities laws (collectively, “forward-looking statements”). These statements appear in a number of places in this news release and include statements regarding our intent, or the beliefs or current expectations of our officers and directors, including PEA results (including NPV, IRR and pay-back period, margins, and EBITDA); potential amounts of graphite production; specifications of the Kilbourne project; future EXIM lending; use of proceeds from EXIM lending; initial construction capital; future ESM cashflow; graphite outputs; exploration potential; near term production pathway; qualification sales production commencing in Q4 2025 with customer qualifications commencing Q1 2026; the demonstration facility significantly de-risks the Kilbourne Project, accelerates time-to-market, and provides early validation of Titan’s downstream processing strategy; Feasibility Study in 2026 with targeted start of construction in 2027; Project expected to create approximately 160 additional permanent positions, establishing a total workforce of over 300 employees across ESM operations in upstate New York, while generating tax revenue and local economic benefits for St. Lawrence County and New York State; ongoing production from the Empire State Mine provides cash flow stability, with production expected to grow incrementally; exploration potential across Titan’s land package and operational synergies with the Kilbourne Project further enhance value and reduce execution risk; Titan is poised to be able to supply nearly half of the nation’s natural graphite demand through a fully integrated operation in New York State; we are building a U.S.-anchored critical minerals platform with clear, long-term growth; Titan will advance the project to feasibility, supported by additional drilling, expanded metallurgical testing, site-specific engineering, and environmental permitting programs. Pilot-scale purification and downstream test work will generate product samples to secure offtake agreements, further de-risking commercialization and positioning Kilbourne as a cornerstone of U.S. graphite supply; operational parameters of the Kilbourne Project Study; economic highlights of the Kilbourne Project Study; commodity input pricing; Initial, expansion and sustaining capital costs; Project All-in Operating Costs. When used in this news release words such as “to be”, “will”, “planned”, “expected”, “potential”, and similar expressions are intended to identify these forward-looking statements.

Although the Company believes that the expectations reflected in such forward-looking statements and/or information are reasonable, undue reliance should not be placed on forward-looking statements since the Company can give no assurance that such expectations will prove to be correct. These statements involve known and unknown risks, uncertainties and other factors that may cause actual results or events to vary materially from those anticipated in such forward-looking statements, including risks relating to cost increases for capital and operating costs; risks of shortages and fluctuating costs of equipment or supplies; risks relating to fluctuations in the price of zinc and graphite; the inherently hazardous nature of mining-related activities; potential effects on our operations of environmental regulations in New York State; risks due to legal proceedings; and risks related to operation of mining projects generally and the risks, uncertainties and other factors identified in the Company’s periodic filings with Canadian securities regulators.

Such forward-looking statements are based on various assumptions, including assumptions made with regard to our forecasts and expected cash flows; our projected capital and operating costs; our expectations regarding mining and metallurgical recoveries; mine life and production rates; that laws or regulations impacting mining activities will remain consistent; our approved business plans; our mineral resource estimates and results of the PEA; our experience with regulators; political and social support of the mining industry in New York State; our experience and knowledge of the New York State mining industry and our expectations of economic conditions and the price of zinc and graphite; demand for graphite; exploration results; the ability to secure adequate financing (as needed); the Company maintaining its current strategy and objectives; and the Company’s ability to achieve its growth objectives. While the Company considers these assumptions to be reasonable, based on information currently available, they may prove to be incorrect.

Except as required by applicable law, we assume no obligation to update or to publicly announce the results of any change to any forward-looking statement contained herein to reflect actual results, future events or developments, changes in assumptions or changes in other factors affecting the forward-looking statements. If we update any one or more forward-looking statements, no inference should be drawn that we will make additional updates with respect to those or other forward-looking statements. You should not place undue importance on forward-looking statements and should not rely upon these statements as of any other date. All forward-looking statements contained in this news release are expressly qualified in their entirety by this cautionary statement.

Past performance is not an indicator of future returns. NIA is not an investment advisor and does not provide investment advice. Always do your own research and make your own investment decisions. This message is for informational and educational purposes only and does not provide investment advice.